China in Focus: A great rebalancing

17 April 2026

Key takeaways

-

Stoking domestic demand and rebalancing trade are key priorities for China’s government this year.

-

Fixed asset investment is showing signs of a recovery while manufacturing may gain from reduced tariff uncertainty.

-

Fiscal and monetary measures, alongside structural reforms, are expected to support consumption.

China data review (Q1 & March 2026)[@source-wind-hsbc]

-

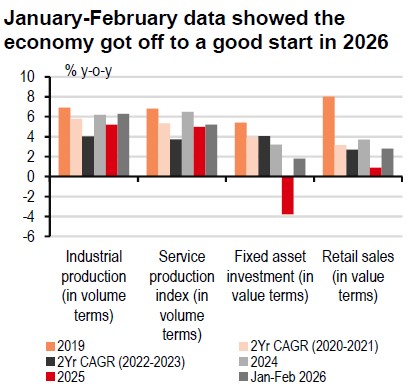

GDP rose by 5% y-o-y in Q1, putting growth on track for this year’s government target, but global geopolitical uncertainties may still pose challenges. Growth was largely helped by outperforming exports in Jan-Feb and accelerated fiscal policy. We expect China to keep its focus on “doing one’s own thing well” with continued policy support, primarily via fiscal policy and new spending tools.

-

Fixed Asset Investment rose 1.6% y-o-y in March. Infrastructure investment remained a bright spot, up 7.4%; however, property continued to drag, with overall investment falling by 11% y-o-y. Nonetheless, some property indicators improved a touch: New primary home sales by volume fell 10% y-o-y versus a 16% decline in Jan-Feb, helped by demand in tier-1 cities.

-

Industrial Production rose 5.7% y-o-y in March, softer than Jan-Feb owing to lower exports in March, Chinese New Year effects and drags from the Middle East conflict. Sector data indicates resilience in electronics and transport goods, which supported the better-than-expected headline growth. This underscores China’s strong price and quality competitiveness across related sectors.

-

Retail Sales slowed to 1.7% y-o-y in March, mainly weighed down by a high base and a pullback in the scale of trade-in subsidies. Auto sales (-12% y-o-y) remained the key drag as the purchase tax for new energy vehicles was adjusted from a full exemption to a 50% reduction this year. Communications appliances posted double-digit growth, remaining a structural bright spot.

-

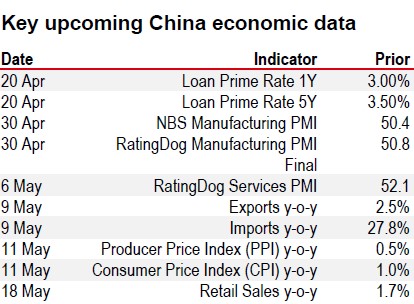

PPI returned to the positive y-o-y territory for the first time since October 2022, rising 0.5% y-o-y in March. The primary drivers were the energy and non-ferrous metals sectors along with the ongoing anti-involution campaign. On the consumer side, CPI rose 1.0% y-o-y, partly lifted by vehicle fuel prices while gold products likely also remained a key driver.

-

Exports eased to 2.5% y-o-y in March amidst an unfavourable base and distortions caused by some seasonal factors. However, imports rose by 27.8% y-o-y, likely driven by domestic policy push for technological upgrading and infrastructure investment, as well as strong global AI-related demand.

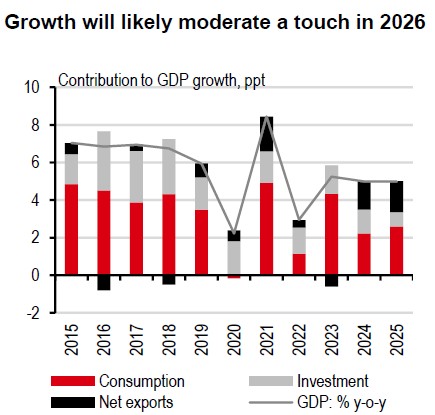

A great rebalancing

China’s 2026 growth target of 4.5-5.0% reflects a maturing economy and a strategic pivot towards sustainable, high-quality growth. The government’s focus is clear: domestic demand will be the primary engine, while there will be deliberate efforts to balance trade.

On the up

Recent data show fixed asset investment (FAI) is starting to recover after a rare contraction in 2025 across manufacturing, infrastructure, and property. The turnaround is driven by new government funding, RMB800bn in policy-related financial tools, and front-loaded bond quotas from the 2026 budget. Local governments now have more “seed capital” for infrastructure and urban development – last year’s RMB500bn unlocked RMB7trn in projects (people.com.cn, 2 November 2025), and a similar multiplier is expected this year. Ongoing local government debt swaps and repayments of local arrears should further ease liquidity pressure, boost business confidence, and attract more private capital for public projects.

Manufacturing investment stands to benefit from reduced tariff uncertainty: following recent US policy changes – including the removal of International Emergency Economic Powers Act (IEEPA) tariffs and the introduction of a Section 122 10% tariff – China’s trade-weighted tariff rate has dropped by c10 percentage points to c25%, narrowing the gap with other major exporters. Diplomatic momentum is also building: China’s foreign minister has described 2026 as a potential ‘landmark year’ for US-China relations, with up to four presidential meetings anticipated, starting with President Trump’s visit to China (South China Morning Post, 23 March 2026).

On the consumption side, support will remain robust, with another batch of RMB250bn consumer goods trade-in subsidy and a new RMB100bn fiscal-financial coordination tool to broaden support beyond goods to services and providers. Structural reforms – such as improved social welfare, pension reform, and urbanisation – are also in the pipeline to boost disposable income and raise the share of consumption in GDP over the medium term.

Trade is expected to be more balanced. As outbound direct investment grows, it will partially replace direct exports, but supply chain-related trade will expand. During the National People’s Congress in March, officials pledged to “balance trade” and expand imports, e.g., agricultural products, premium consumer goods, and advanced equipment and key components (Gov.cn, 7 March). The government’s commitment to further opening-up, especially in services sectors, should help reduce frictions.

Source: Wind, HSBC

Source: Wind, HSBC

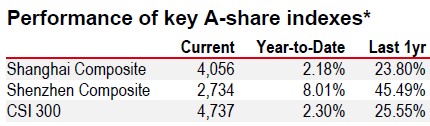

Source: LSEG Eikon

* Past performance is not an indication of future returns

Source: LSEG Eikon. As of 16 April 2026, market close

Related Insights

Disclosure appendix

Additional disclosures

1. This report is dated as at 17 April 2026.

2. All market data included in this report are dated as at close 15 April 2026, unless a different date and/or a specific time of day is indicated in the report.

3. HSBC has procedures in place to identify and manage any potential conflicts of interest that arise in connection with its Research business. HSBC's analysts and its other staff who are involved in the preparation and dissemination of Research operate and have a management reporting line independent of HSBC's Investment Banking business. Information Barrier procedures are in place between the Investment Banking, Principal Trading, and Research businesses to ensure that any confidential and/or price sensitive information is handled in an appropriate manner.

4. You are not permitted to use, for reference, any data in this document for the purpose of (i) determining the interest payable, or other sums due, under loan agreements or under other financial contracts or instruments, (ii) determining the price at which a financial instrument may be bought or sold or traded or redeemed, or the value of a financial instrument, and/or (iii) measuring the performance of a financial instrument or of an investment fund.

Disclaimer

This document is prepared by The Hongkong and Shanghai Banking Corporation Limited (‘HBAP’), 1 Queen’s Road Central, Hong Kong. HBAP is incorporated in Hong Kong and is part of the HSBC Group. This document is distributed by HSBC Continental Europe, HBAP, HSBC Bank (Singapore) Limited, HSBC Bank (Taiwan) Limited, HSBC Bank Malaysia Berhad (198401015221 (127776-V))/HSBC Amanah Malaysia Berhad (200801006421 (807705-X)), The Hongkong and Shanghai Banking Corporation Limited, India (HSBC India), HSBC Bank Middle East Limited, HSBC UK Bank plc, HSBC Bank plc, Jersey Branch, and HSBC Bank plc, Guernsey Branch, HSBC Private Bank (Suisse) SA, HSBC Private Bank (Suisse) SA DIFC Branch, , HSBC Financial Services (Lebanon) SAL, HSBC Private banking (Luxembourg) SA, and The Hongkong and Shanghai Banking Corporation Limited (collectively, the “Distributors”) to their respective clients. This document is for general circulation and information purposes only. This document is not prepared with any particular customers or purposes in mind and does not take into account any investment objectives, financial situation or personal circumstances or needs of any particular customer. HBAP has prepared this document based on publicly available information at the time of preparation from sources it believes to be reliable but it has not independently verified such information. The contents of this document are subject to change without notice. HBAP and the Distributors are not responsible for any loss, damage or other consequences of any kind that you may incur or suffer as a result of, arising from or relating to your use of or reliance on this document. HBAP and the Distributors give no guarantee, representation or warranty as to the accuracy, timeliness or completeness of this document. This document is not investment advice or recommendation nor is it intended to sell investments or services or solicit purchases or subscriptions for them. You should not use or rely on this document in making any investment decision. HBAP and the Distributors are not responsible for such use or reliance by you. You should consult your professional advisor in your jurisdiction if you have any questions regarding the contents of this document. You should not reproduce or further distribute the contents of this document to any person or entity, whether in whole or in part, for any purpose. This document may not be distributed to any jurisdiction where its distribution is unlawful.

The following statement is only applicable to HSBC Bank (Taiwan) Limited with regard to how the publication is distributed to its customers: HSBC Bank (Taiwan) Limited (“the Bank”) shall fulfill the fiduciary duty act as a reasonable person once in exercising offering/conducting ordinary care in offering trust services/business. However, the Bank disclaims any guaranty on the management or operation performance of the trust business.

The following statement is only applicable to by HSBC Bank Australia with regard to how the publication is distributed to its customers: This document is distributed by HSBC Bank Australia Limited ABN 48 006 434 162, AFSL/ACL 232595 (HBAU). HBAP has a Sydney Branch ARBN 117 925 970 AFSL 301737.The statements contained in this document are general in nature and do not constitute investment research or a recommendation, or a statement of opinion (financial product advice) to buy or sell investments. This document has not taken into account your personal objectives, financial situation and needs. Because of that, before acting on the document you should consider its appropriateness to you, with regard to your objectives, financial situation, and needs.

Important Information about the Hongkong and Shanghai Banking Corporation Limited, India (“HSBC India”)

HSBC India is a branch of The Hongkong and Shanghai Banking Corporation Limited. HSBC India is a distributor of mutual funds and referrer of investment products from third party entities registered and regulated in India. HSBC India does not distribute investment products to those persons who are either the citizens or residents of United States of America (USA), Canada, Australia or New Zealand or any other jurisdiction where such distribution would be contrary to law or regulation.

Singapore

In Singapore, this document:

- has not been reviewed by any regulatory authority in Singapore or any other jurisdiction.

- is issued by HSBC Bank (Singapore) Limited (the "Bank") in the conduct of its business in Singapore and is for general information.

- is only meant for the person who received it and should not be copied or shared with others, either fully or partially, for any reason.

- must not be sent to the United States, Canada or Australia or to any other jurisdiction where sharing it is illegal. If someone uses or copies this document or video without permission, they could face legal action.

- gives a broad overview of the current economic environment and is not meant to be investment research or advice or a recommendation to buy or sell investments. Some parts might talk about future events, but these are just predictions and not promises nor guarantees of future performance or events. Actual results might turn out differently due to various reasons. The Bank is not responsible for updating these predictions or explaining why actual results could differ from those predictions.

- does not create any contracts and isn’t meant as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction where it is not legal. Investments can increase or decrease in value, and you might not get back the amount you initially invested. Investments come with market risks, so it is important to read all investment-related documents carefully. The opinions shared are from the HSBC Global Investment Committee at the time of creating this document or video and reflect its global perspective, which might differ from local views of the Bank. These opinions can change anytime and might not match HSBC Asset Management‘s current portfolios’ composition. HSBC Asset Management manages individual portfolios based on each client’s objectives, risk preferences, time horizon, and market conditions.

- has not been created following legal requirements for independent investment research and is not subject to any prohibition on dealing ahead of its dissemination.

- is not meant to offer accounting, legal or tax advice. Before making any investment decision, consider consulting a financial adviser. If you decide not to seek advice, carefully assess if the investment product is suitable for you. It is recommended to obtain appropriate professional advice when needed. Investing overseas can lead to changes in the value of your investments due to currency exchange rates, which may cause them to rise or fall. Emerging markets are riskier and more unpredictable compared to established markets. These economies often depend heavily on international trade and can be adversely impacted by trade barriers, currency controls, adjustments in currency values, the economic conditions of their trading partners and other protective measures imposed by those partners. We are not responsible for the accuracy and/or completeness of any third-party information obtained from sources we believe to be reliable but have not independently verified.

Mainland China

In mainland China, this document is distributed by HSBC Bank (China) Company Limited (“HBCN”) and HSBC FinTech Services (Shanghai) Company Limited to its customers for general reference only. This document is not, and is not intended to be, for the purpose of providing securities and futures investment advisory services or financial information services, or promoting or selling any wealth management product. This document provides all content and information solely on an "as-is/as-available" basis. You SHOULD consult your own professional adviser if you have any questions regarding this document.

The material contained in this document is for general information purposes only and does not constitute investment research or advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. HSBC India does not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. Investments are subject to market risk, read all investment related documents carefully.

© Copyright 2026. The Hongkong and Shanghai Banking Corporation Limited, ALL RIGHTS RESERVED.

No part of this document may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of The Hongkong and Shanghai Banking Corporation Limited.

Important information on sustainable investing

“Sustainable investments” include investment approaches or instruments which consider environmental, social, governance and/or other sustainability factors (collectively, “sustainability”) to varying degrees. Certain instruments we include within this category may be in the process of changing to deliver sustainability outcomes.

There is no guarantee that sustainable investments will produce returns similar to those which don’t consider these factors. Sustainable investments may diverge from traditional market benchmarks.

In addition, there is no standard definition of, or measurement criteria for sustainable investments, or the impact of sustainable investments (“sustainability impact”). Sustainable investment and sustainability impact measurement criteria are (a) highly subjective and (b) may vary significantly across and within sectors.

HSBC may rely on measurement criteria devised and/or reported by third party providers or issuers. HSBC does not always conduct its own specific due diligence in relation to measurement criteria. There is no guarantee: (a) that the nature of the sustainability impact or measurement criteria of an investment will be aligned with any particular investor’s sustainability goals; or (b) that the stated level or target level of sustainability impact will be achieved.

Sustainable investing is an evolving area and new regulations may come into effect which may affect how an investment is categorised or labelled. An investment which is considered to fulfil sustainable criteria today may not meet those criteria at some point in the future.