14 May 2026

Key takeaways

-

There have been some signs of resilience heading into the latest shock…

-

…but sentiment has tumbled as price pressures intensify.

-

The BoE is focused on the risk that this latest bout of inflation becomes embedded in wages.

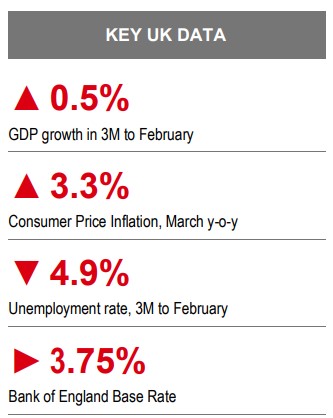

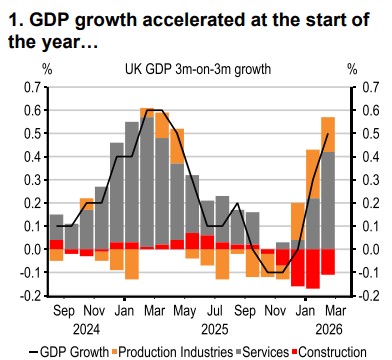

The UK economy reported the fastest pace of growth since April 2025 in the three months to February. That means the UK had a firm base heading into the latest period of uncertainty. In fact, activity surveys in April continued to report a degree of demand momentum. The manufacturing sector PMI jumped to 53.7, bolstered by new order growth, while the services sector reported higher business activity with a PMI of 52.0. However, reports of inventory accumulation ahead of expected supply disruption likely overstate activity momentum. Retail sales demand was also flattered by a degree of panic buying of motor fuel, +3.2% m-o-m in March, while overall, retail sales volumes excluding fuel grew a meagre 0.2% m-o-m.

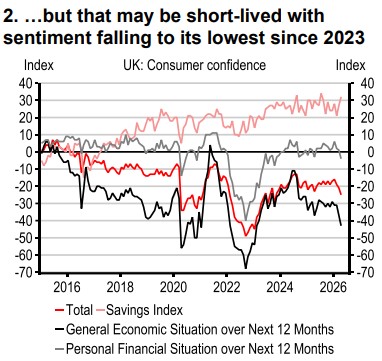

Elsewhere, consumer confidence fell further in April, taking sentiment to its lowest level in more than two years. It’s no surprise that facing another inflation shock has left consumers particularly cautious about the future state of the economy, and their own personal financial situations, for the latter, the net balance fell back negative. Savings intentions also rose, new-buyer enquiries for home purchases fell to their lowest level since August 2023 in March, and medium-term inflation expectations have spiked higher.

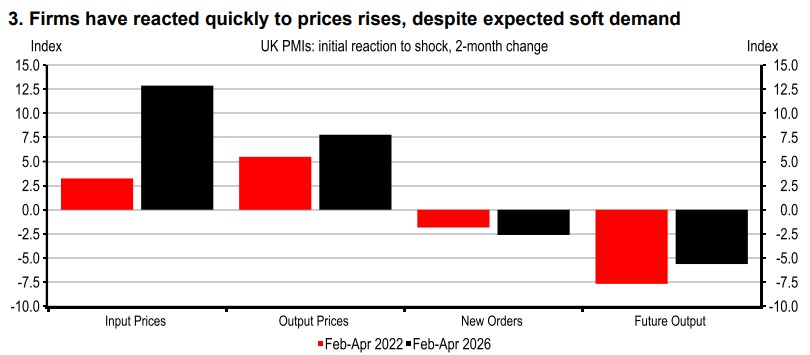

While the initial volatility across both household and business surveys may subside in the coming months, energy prices and supply disruption will continue to pass through the global economy for a while yet. And early indicators suggest agents have a greater sensitivity to price rises with a degree of pass-through evident despite the prospect of softer demand – see chart.

For the Bank of England (BoE), the extent to which the latest price shock translates into domestically driven inflation will determine the policy response. In our view, the risk of any second-round inflationary effects is smaller than in recent years, and at its latest policy meeting, the BoE seemed to agree. Nonetheless, the BoE’s scenarios showed how different assumptions on second-round effects, namely through higher wage growth, would require greater interest rate hikes. Such effects can take well over a year to materialise, but if the central bank were to wait for that, it may need to respond more aggressively than otherwise needed; therefore, hikes sooner to mitigate the risk are more likely.

For now, market expectations of rate hikes have tightened financial conditions, meaning the BoE may opt to wait and see, in the hope of greater clarity on the outcome of the Middle East conflict, and to see how households and businesses respond.

That being said, unless there is a swift resolution to the conflict and a reopening of the Strait of Hormuz, we expect the BoE will need to raise Bank Rate in the summer. The rate of inflation is set to accelerate, and with households and businesses more sensitive to higher prices, we think policymakers are likely to opt to lean against the risk that higher inflation now becomes embedded within household and business price expectations.

Related Insights

Disclosure appendix

This publication has been prepared by HSBC Bank plc (“HBEU”) which is part of the HSBC Group. It is intended for information purposes only and is not intended for further distribution whether through the press or via other means. Nothing in this publication constitutes or is to be construed as an offer to buy or sell or a solicitation of an offer to buy or sell the securities or other investment products mentioned in it and/or to participate in any trading strategy. Information in this publication is general and should not be construed as investment advice or guidance as it has been prepared without taking account of the objectives, financial situation or needs of any particular investor. Investors should, accordingly, before acting on any information contained herein, consider the appropriateness of the information having regard to their objectives, financial situation and needs and should, if necessary, seek professional investment and/or tax advice.

Certain investment products mentioned in this publication may not be eligible for sale in some countries or territories and may not be suitable for all types of investors. Investors should consult with their HSBC representative regarding the suitability of any investment products mentioned taking into account their specific investment objectives, financial situation and/or particular needs before making a commitment to purchase any investment products. The value of and the income produced by investment products mentioned in this publication may fluctuate so an investor may get back less than originally invested. Certain high-volatility investments can be subject to sudden and/or large falls in value that could equal or exceed the amount invested. Value and income from investment products may be adversely affected by exchange rates, interest rates, or other factors. Past performance of a particular investment product is not indicative of future results. When an investment is denominated in a currency other than the local currency of an investor, changes in the exchange rates may have an adverse effect on the value, price or income of that investment. Where there is no recognised market for an investment, it may be difficult for an investor to sell the investment or to obtain reliable information about its value or the extent of the risk associated with it.

This publication may contain forward-looking statements which are, by their nature, subject to significant risks and uncertainties. Any such statements are projections and are used for illustration purpose only. Customers are reminded that there can be no assurance that economic conditions described herein will remain in the future. Actual results may differ materially from the forecasts and/or estimates. No assurance is given that expectations reflected in any forward-looking statements will prove to have been correct or come to fruition, and you are cautioned not to place undue reliance on such statements. No obligation is undertaken to publicly update or revise any forward-looking statements contained in this publication or in any other related publication whether as a result of new information, future events or otherwise.

This publication is distributed by HBEU, its affiliates and its associated entities (together, the “HBEU entities”) to their customers. No HBEU entity is responsible for any loss, damage or other consequence of any kind that may be incurred or suffered as a result of, arising from, or relating to any use or reliance on this publication. No HBEU entity gives any guarantee as to the accuracy, timeliness or completeness of this publication. Whether, or in what time frame, an update of any information contained herein will be published is not determined in advance. You should consult your own professional advisor if you have any questions regarding the content of this publication.

HBEU entities and their respective officers and/or employees may have interests in any products referred to in this publication by acting in various roles including as distributor, holder of principal positions, adviser or lender. HBEU entities and their respective officers and employees may receive fees, brokerage or commissions for acting in those capacities. In addition, HBEU entities and their respective officers and/or employees may buy or sell products as principal or agent and may effect transactions which are not consistent with the information set out in this publication.

Additional disclosures

1. This report is dated as at 13 May 2026.

2. All market data included in this report are dated as at close 12 May 2026, unless a different date and/or a specific time of day is indicated in the report.

3. HBEU has procedures in place to identify and manage any potential conflicts of interest that arise in connection with its research business. HBEU’s analysts and its other staff who are involved in the preparation and dissemination of research operate and have a management reporting line independent of HBEU’s investment business. Information barrier procedures are in place between the investment banking, principal trading and research businesses to ensure that any confidential and/or price sensitive information is handled in an appropriate manner.

4. Recipients of this publication are not permitted to use, for reference, any data in this publication for the purpose of (i) determining the interest payable, or other sums due, under loan agreements or under other financial contracts or instruments, (ii) determining the price at which a financial instrument may be bought, sold, traded or redeemed, or the value of a financial instrument, and/or (iii) measuring the performance of a financial instrument.

Disclaimer

This document is prepared by The Hongkong and Shanghai Banking Corporation Limited (‘HBAP’), 1 Queen’s Road Central, Hong Kong. HBAP is incorporated in Hong Kong and is part of the HSBC Group. This document is distributed by HSBC Continental Europe, HBAP, HSBC Bank (Singapore) Limited, HSBC Bank (Taiwan) Limited, HSBC Bank Malaysia Berhad (198401015221 (127776-V))/HSBC Amanah Malaysia Berhad (200801006421 (807705-X)), The Hongkong and Shanghai Banking Corporation Limited, India (HSBC India), HSBC Bank Middle East Limited, HSBC UK Bank plc, HSBC Bank plc, Jersey Branch, and HSBC Bank plc, Guernsey Branch, HSBC Private Bank (Suisse) SA, HSBC Private Bank (Suisse) SA DIFC Branch, , HSBC Financial Services (Lebanon) SAL, HSBC Private banking (Luxembourg) SA, and The Hongkong and Shanghai Banking Corporation Limited (collectively, the “Distributors”) to their respective clients. This document is for general circulation and information purposes only. This document is not prepared with any particular customers or purposes in mind and does not take into account any investment objectives, financial situation or personal circumstances or needs of any particular customer. HBAP has prepared this document based on publicly available information at the time of preparation from sources it believes to be reliable but it has not independently verified such information. The contents of this document are subject to change without notice. HBAP and the Distributors are not responsible for any loss, damage or other consequences of any kind that you may incur or suffer as a result of, arising from or relating to your use of or reliance on this document. HBAP and the Distributors give no guarantee, representation or warranty as to the accuracy, timeliness or completeness of this document. This document is not investment advice or recommendation nor is it intended to sell investments or services or solicit purchases or subscriptions for them. You should not use or rely on this document in making any investment decision. HBAP and the Distributors are not responsible for such use or reliance by you. You should consult your professional advisor in your jurisdiction if you have any questions regarding the contents of this document. You should not reproduce or further distribute the contents of this document to any person or entity, whether in whole or in part, for any purpose. This document may not be distributed to any jurisdiction where its distribution is unlawful.

The following statement is only applicable to HSBC Bank (Taiwan) Limited with regard to how the publication is distributed to its customers: HSBC Bank (Taiwan) Limited (“the Bank”) shall fulfill the fiduciary duty act as a reasonable person once in exercising offering/conducting ordinary care in offering trust services/business. However, the Bank disclaims any guaranty on the management or operation performance of the trust business.

The following statement is only applicable to by HSBC Bank Australia with regard to how the publication is distributed to its customers: This document is distributed by HSBC Bank Australia Limited ABN 48 006 434 162, AFSL/ACL 232595 (HBAU). HBAP has a Sydney Branch ARBN 117 925 970 AFSL 301737.The statements contained in this document are general in nature and do not constitute investment research or a recommendation, or a statement of opinion (financial product advice) to buy or sell investments. This document has not taken into account your personal objectives, financial situation and needs. Because of that, before acting on the document you should consider its appropriateness to you, with regard to your objectives, financial situation, and needs.

Important Information about the Hongkong and Shanghai Banking Corporation Limited, India (“HSBC India”)

HSBC India is a branch of The Hongkong and Shanghai Banking Corporation Limited. HSBC India is a distributor of mutual funds and referrer of investment products from third party entities registered and regulated in India. HSBC India does not distribute investment products to those persons who are either the citizens or residents of United States of America (USA), Canada, Australia or New Zealand or any other jurisdiction where such distribution would be contrary to law or regulation.

Singapore

In Singapore, this document:

• has not been reviewed by any regulatory authority in Singapore or any other jurisdiction.

• is issued by HSBC Bank (Singapore) Limited (the "Bank") in the conduct of its business in Singapore and is for general information.

• is only meant for the person who received it and should not be copied or shared with others, either fully or partially, for any reason.

• must not be sent to the United States, Canada or Australia or to any other jurisdiction where sharing it is illegal. If someone uses or copies this document or video without permission, they could face legal action.

• gives a broad overview of the current economic environment and is not meant to be investment research or advice or a recommendation to buy or sell investments. Some parts might talk about future events, but these are just predictions and not promises nor guarantees of future performance or events. Actual results might turn out differently due to various reasons. The Bank is not responsible for updating these predictions or explaining why actual results could differ from those predictions.

• does not create any contracts and isn’t meant as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction where it is not legal. Investments can increase or decrease in value, and you might not get back the amount you initially invested. Investments come with market risks, so it is important to read all investment-related documents carefully. The opinions shared are from the HSBC Global Investment Committee at the time of creating this document or video and reflect its global perspective, which might differ from local views of the Bank. These opinions can change anytime and might not match HSBC Asset Management‘s current portfolios’ composition. HSBC Asset Management manages individual portfolios based on each client’s objectives, risk preferences, time horizon, and market conditions.

• has not been created following legal requirements for independent investment research and is not subject to any prohibition on dealing ahead of its dissemination.

• is not meant to offer accounting, legal or tax advice. Before making any investment decision, consider consulting a financial adviser. If you decide not to seek advice, carefully assess if the investment product is suitable for you. It is recommended to obtain appropriate professional advice when needed.

Investing overseas can lead to changes in the value of your investments due to currency exchange rates, which may cause them to rise or fall. Emerging markets are riskier and more unpredictable compared to established markets. These economies often depend heavily on international trade and can be adversely impacted by trade barriers, currency controls, adjustments in currency values, the economic conditions of their trading partners and other protective measures imposed by those partners.

We are not responsible for the accuracy and/or completeness of any third-party information obtained from sources we believe to be reliable but have not independently verified.

Mainland China

In mainland China, this document is distributed by HSBC Bank (China) Company Limited (“HBCN”) and HSBC FinTech Services (Shanghai) Company Limited to its customers for general reference only. This document is not, and is not intended to be, for the purpose of providing securities and futures investment advisory services or financial information services, or promoting or selling any wealth management product. This document provides all content and information solely on an "as-is/as-available" basis. You SHOULD consult your own professional adviser if you have any questions regarding this document.

The material contained in this document is for general information purposes only and does not constitute investment research or advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. HSBC India does not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. Investments are subject to market risk, read all investment related documents carefully.

© Copyright 2026. The Hongkong and Shanghai Banking Corporation Limited, ALL RIGHTS RESERVED.

No part of this document may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of The Hongkong and Shanghai Banking Corporation Limited.

Important information on sustainable investing

“Sustainable investments” include investment approaches or instruments which consider environmental, social, governance and/or other sustainability factors (collectively, “sustainability”) to varying degrees. Certain instruments we include within this category may be in the process of changing to deliver sustainability outcomes. There is no guarantee that sustainable investments will produce returns similar to those which don’t consider these factors. Sustainable investments may diverge from traditional market benchmarks.

In addition, there is no standard definition of, or measurement criteria for sustainable investments, or the impact of sustainable investments (“sustainability impact”). Sustainable investment and sustainability impact measurement criteria are (a) highly subjective and (b) may vary significantly across and within sectors.

HSBC may rely on measurement criteria devised and/or reported by third party providers or issuers. HSBC does not always conduct its own specific due diligence in relation to measurement criteria. There is no guarantee: (a) that the nature of the sustainability impact or measurement criteria of an investment will be aligned with any particular investor’s sustainability goals; or (b) that the stated level or target level of sustainability impact will be achieved.

Sustainable investing is an evolving area and new regulations may come into effect which may affect how an investment is categorised or labelled. An investment which is considered to fulfil sustainable criteria today may not meet those criteria at some point in the future.